Business Owners in Building and Construction Need to Act.

Note: The measures discussed in this article were announced in the 2026–27 Federal Budget on 12 May 2026. They are proposals, not yet enacted law. Draft legislation is expected later this year. I am a Registered Business Valuer, not a tax adviser. Nothing in this article constitutes tax advice. You should speak with your accountant or tax adviser about your specific circumstances.

I have been in business valuation for more than 25 years. In that time, I have watched business owners make expensive decisions based on incomplete information — not because they were careless, but because nobody told them what was coming until it was too late.

Last week’s Federal Budget is one of those moments. If you own a business in building, construction, or the trades, and you are thinking about selling — whether next year, in five years, or at some point before you retire — what was announced on 12 May 2026 directly affects how much of those sale proceeds you will keep.

I want to be straightforward with you about what the Budget actually says, what it means in practical terms, and what you can do about it. Not alarm you. Not sell you something. Just give you the information you need to make good decisions.

What the Government Has Proposed

Since 1999, if you sold a business asset — including shares in your company — after holding it for more than twelve months, you were entitled to a 50 per cent discount on the capital gain before paying tax. That concession has been a cornerstone of business exit planning for a generation.

The Treasurer announced that from 1 July 2027, that 50 per cent discount will be abolished. In its place, the Government proposes two things: cost base indexation, which adjusts the original purchase price for inflation; and a 30 per cent minimum tax rate on the real capital gain that remains after indexation.

| The CGT reforms will only apply to gains arising after 1 July 2027. The Government’s own budget fact sheet confirms this directly. Gains accrued before that date are protected under the transitional arrangements — but only if the split is correctly established. |

That phrase — only applies to gains arising after 1 July 2027 — is the heart of this. It is not that the new rules do not apply to you because you already own your business. They will apply to every dollar of growth that occurs in your business after that date. The question is whether the value in your business that is already built — the years of work, the client relationships, the contracts, the reputation — is properly accounted for before the clock resets.

How the Transitional Mechanism Actually Works

The Budget creates what is effectively a value split at a single date: 1 July 2027. Every asset you own on that date — including shares in your company — will have its gain divided into two periods.

The gain from when you acquired the asset through to 1 July 2027 is calculated under the old rules. The 50 per cent discount applies to that portion. The gain from 1 July 2027 onwards is calculated under the new rules — indexation and the 30 per cent MINIMUM tax.

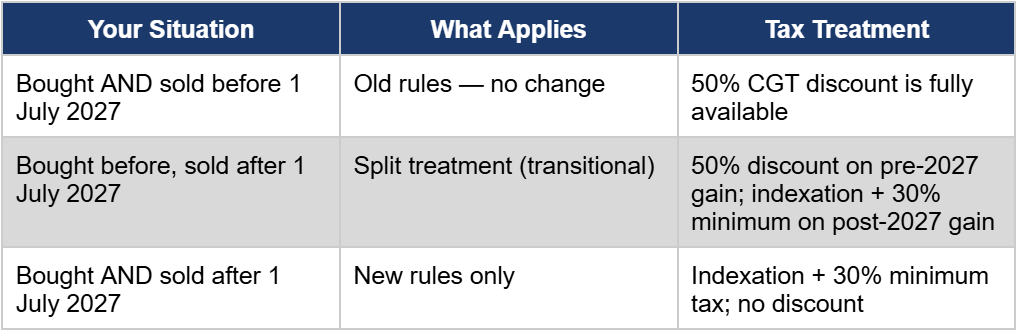

Here is how the Budget describes the three scenarios business owners face:

Most business owners who are reading this fall into the middle row. You own your business now. You are not selling tomorrow. But when you do sell — in two years, in seven years, in fifteen years — 1 July 2027 becomes the dividing line between two separate tax regimes. What is taxed leniently, and what is taxed at the new, higher effective rate.

The Number That Determines Your Tax: How the July 2027 Value Is Established

This is the part that most business owners are not hearing clearly enough, so I want to be precise about it.

To calculate how much of your eventual gain falls under the old rules versus the new rules, someone has to establish what your business was worth on July 2027. The Budget provides two options for doing this.

The first is a formal independent valuation. The second is a government-provided apportionment formula, which estimates the 1 July 2027 value by working backwards from the asset’s cost base and growth rate over the holding period.

| The formula assumes your business has grown at a steady, consistent rate since the day you acquired it. If that does not reflect reality — and for most building and construction businesses, it does not — the formula will produce a number that is wrong. And a lower 1 July 2027 value means more of your future gain falls under the new rules. |

Think about what drives value in your kind of business. You may have a project pipeline that grew significantly in the first few years. You may have brought on key staff or moved your role to part-time after a period of owner dependency. Your contracts may have lengthened, or your margins improved. You may have built genuine goodwill in a specialised niche — civil works, commercial fitout, residential construction — that a formula will not see.

A formula calculates. A valuation understands. For a business like yours, those are not the same thing.

Pitcher Partners, one of Australia’s leading advisory firms, made this point clearly in their analysis of the Budget: where assets are complex, unique, or closely held, establishing an appropriate market value may be inherently difficult, particularly where value is driven by intangibles. A prescribed formula may not appropriately capture the value of the particular asset at the 1 July 2027 test date.

Your goodwill is not a line item in a formula. Your reputation in the market is not captured by a growth rate percentage. But it is captured in a properly conducted, IVS-compliant business valuation.

What Has Not Changed — The Small Business CGT Concessions

I want to be clear about one thing that has generated some confusion. The four small business CGT concessions — the 15-year exemption, the retirement exemption, the active asset reduction, and the rollover provision — have not been removed (YET). The Budget explicitly confirms this.

If you qualify for those concessions when you sell, they remain available to you. This matters because some business owners I have spoken with in recent days have assumed the Budget swept everything away. It has not. What it has done is change the rate at which gains that do not qualify for those concessions — or that exceed the eligibility thresholds — will be taxed.

There is also a structural issue worth flagging, particularly for those operating through a family discretionary trust. From 1 July 2028, the Budget proposes a 30 per cent MINIMUM tax on discretionary trust taxable income. The Government has offered three years of rollover relief from 1 July 2027 for those who wish to restructure. That is a separate conversation — and one that requires your accountant and a current business valuation before any restructuring decision is made.

Why the Timing of a Valuation Matters

Let me address the practical question directly: Does this mean you need a valuation done right now, immediately, in the next few weeks?

Not necessarily. The Budget papers confirm that the 1 July 2027 value is determined at the time you eventually sell — in your tax return for the year of sale, not before. You are not required to obtain a valuation before 1 July 2027.

Here is the truth about retrospective valuations. They are pretty common, in fact, most valuations occur after the “date”. A valuation prepared close to the relevant date, with contemporaneous financial records and a current market assessment, is a fundamentally stronger document than one reconstructed years later from historical data alone.

In my experience, the business owners who are best positioned when they sell are the ones who understood what their business was worth before they needed to know. Not in crisis, not under pressure, not scrambling to establish a baseline after the fact.

The window between now and 1 July 2027 may be the right time to establish that baseline — whilst your financials are current, whilst market conditions are observable, and whilst there is no pressure to produce a number on someone else’s timeline. But don’t be rushed into cheap, speedy valuations out of fear.

Who Should Be Having This Conversation Now

Not every business owner needs to act immediately. But if any of the following applies to you, a valuation conversation is worth having before June 2027.

You are planning to sell within the next five to ten years and have not established a current market value for your business. You operate through a discretionary trust and have not yet assessed the impact of the proposed trust tax changes on your structure. You received an unsolicited approach in the past twelve months and are weighing your options. You are in the early stages of succession planning — whether to family, management, or a third-party buyer. Or your accountant has raised the Budget changes with you, and you want an independent, evidence-based view of where your business currently sits.

The conversation does not have to lead to an immediate decision. But the information it produces — a clear, IVS-compliant view of your business value as it stands today — gives you something that neither a formula nor a guess can provide: a defensible position.

A Final Word

Budgets create uncertainty. Uncertainty makes people either rush into decisions or do nothing at all. Neither serves you well here.

What the 2026–27 Budget has done is shift the rules for capital gains on business assets held beyond 1 July 2027. It has not eliminated the value you have already built. It has not removed all concessions. And it has not made selling your business unviable. What it has done is make the established value of your business — as at a specific date — a number that will have direct tax consequences when you eventually exit.

Getting that number right is not a luxury. For building and construction business owners in Queensland, it is now one of the most commercially important decisions you will make in the years ahead.

If you would like to chat about what your business might be worth and what the proposed changes mean for your specific situation, I am happy to have that conversation. There is no cost for the initial discussion, and no obligation beyond it.

Sources: 2026–27 Federal Budget Fact Sheet — Negative Gearing and Capital Gains Tax Reform (budget.gov.au); Budget Paper No. 2; analysis by Corrs Chambers Westgarth, Pitcher Partners, William Buck, PwC Australia, Ashurst, and CPA Australia. All measures are proposals subject to parliamentary approval and may be subject to change. Seek advice from a qualified tax adviser before making financial decisions based on these announcements.